At the end of the Mahabharata war, Yudhishthira, the leader of the Pandavas, is overwhelmed with guilt and grief over the massacre of his relatives. Looking to boost his flagging spirits, Lord Krishna and sage Vyasa advise him to perform the Ashvamedha Yagna—an extravagant and elaborate ceremony meant to demonstrate the suzerainty of Vedic kings.

However, Yudhishthira confides to Krishna that the state treasury is empty because of the war. Krishna then offers a suggestion which would gladden the heart of any multi-asset fund manager—‘fill your coffers with gold (left behind by a king in the Himalayas) and achieve your goals’.

If there is one asset class which carries the weight of antiquity on its shoulders, whose desire is embedded in the very soul of human civilization, and which even today serves as a bulwark against the vicissitudes of fate, it is gold.

While stocks, bonds and other assets flutter in and out of fashion, the almighty gold’s track record as the flagbearer of wealth stretches for over 5,000 years. The ultimate barometer of human progress and prosperity.

Which is why the most prominent investors and institutions around the world sit up and pay attention when the bullion market makes unusual moves.

Shining bright

After a relatively subdued start to the year, gold prices started gathering steam in early March. By April, the precious metal had breached the $2,300 per ounce mark for the first time ever, capping a series of record-shattering moves. As of 9 April, gold had made fresh lifetime highs for eight straight sessions.

Suddenly, a global asset worth $12 trillion was behaving like a jumpy small-cap stock.

The financial cognoscenti scrambled to provide answers.

Some commentators attributed the rally to expectations of interest rate cuts by the US Federal Reserve, which would make the non-yielding yellow metal relatively more attractive.

Others pointed to rising geopolitical tensions, which have always spurred demand for the safe haven asset. But none of these offer a credible explanation for the timing or intensity of the upmove.

The global geopolitical temperature has been feverish for a long time now. As for the Fed’s monetary policy, rate cut projections have actually been scaled back over the past few months due to still-too-hot inflation.

Retail participation in the rally too has been absent. Global gold exchange-traded funds (ETFs) saw outflows for nine consecutive months till February, as per the World Gold Council. In 2024 alone, the outflows have been to the tune of $5.7 billion, with the US and Europe leading the pack.

The Chinese real estate sector is struggling. So many Chinese investors are flocking to gold.

—Ronald-Peter Stöferle

“I think it’s some sort of a new playbook which we are seeing in gold. Real interest rates are very high and yet gold is soaring. We also don’t see too much investor demand for the metal, especially from the western world,” Ronald-Peter Stöferle, managing partner and fund manager at asset management firm Incrementum AG, told Mint on phone from Liechtenstein.

Then what’s driving the rally?

“Chinese demand has been very strong, not only from the central bank…the People’s Bank of China is buying like crazy…but also from private investors because the Chinese real estate sector is struggling. So many Chinese investors are flocking to gold,” he said.

Rest of Asian demand too is holding up well. In fact, China and India are responsible for 50% of gold demand, while overall, the emerging markets account for two-thirds.

“All in all, it’s a very broad bull market…not only in US dollars, gold is at all-time highs in almost every currency,” he said, adding the rally still has legs, though a bit of profit-taking cannot be ruled out.

Tangled ties

View Full Image

What is confounding many market watchers is how other precious metals like silver as well as global equities and even cryptocurrencies are marching to record highs in this ‘everything rally’.

Gold traditionally has an inverse relationship with stocks.

Investors swarm to the precious metal during times of turbulence as a sure-shot way to protect their wealth, while equities are the preferred bet when optimism runs high over the trajectory of economic growth and corporate profits.

For instance, gold shed more than 20% of its value in dollar terms during the 1980s and the 1990s, which were two raging bull market periods for equities.

However, while the S&P500 declined 9% over the first decade of 2000s following the dotcom bubble burst and the 2008-09 financial crisis, gold vaulted by 275%.

So, what explains the current synchronous liftoff?

One reason for these asset classes moving in tandem could be the emergence of high frequency trading.

—Naveen Mathur

“One reason for these asset classes moving in tandem could be the emergence of high frequency trading, in line with the increasing integration of financial markets strengthening correlations between them,” said Naveen Mathur, director—commodities & currencies, AnandRathi Shares and Stock Brokers.

He added that the unprecedented monetary stimulus following the covid-19 crisis has expanded the demand base for assets, driving investors and fund managers towards gold and equities at the same time.

Global experts too say gold and equities moving in conjunction is a central bank-triggered phenomenon.

“We can put this down to a lot of liquidity looking for a home. Equities benefiting from US economic resilience and anticipation of improvements in Europe, which ties in of course with anticipation of falling interest rates. Those arguments apply both to equities and to gold,” Rhona O’Connell, head of market analysis (EMEA & Asia) at American financial services firm StoneX, told Mint.

Which means the gush of liquidity sloshing around in the global financial system is distorting some time-honoured financial correlations, with even a strong dollar not deterring the gold rally.

But no discussion on market distortions is complete without addressing the proverbial 800-pound gorilla in the room.

Chinese checkers

View Full Image

It is remarkable how much impact a single country has on multiple global markets. If you are an analyst tracking anything from copper, crude oil, coal, iron ore and soybeans to lithium, steel or specialty chemicals, you have to keep an eye on China.

The same holds true for bullion.

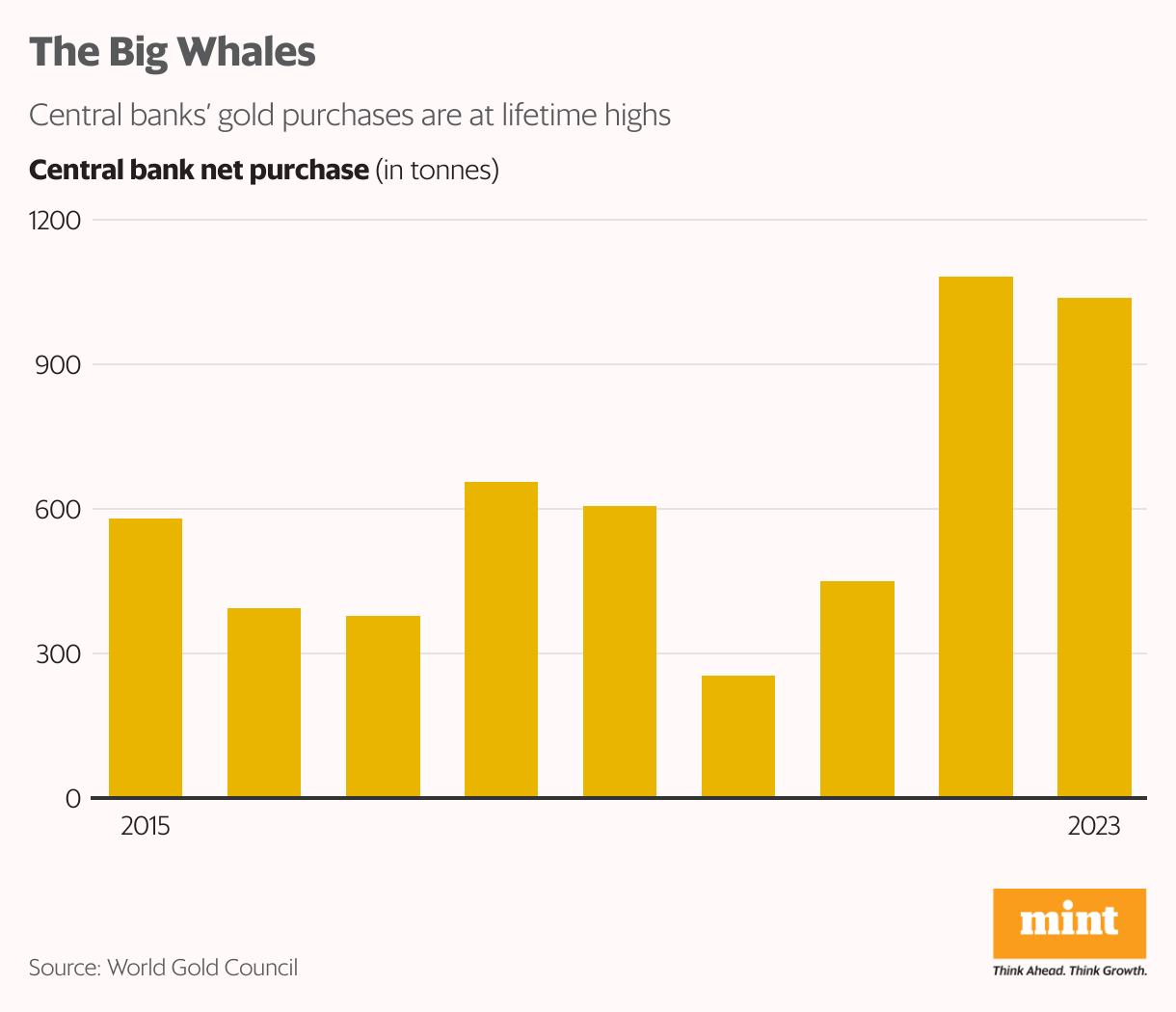

The People’s Bank of China (PBC) has been buying gold with a religious fervour. In 2023, PBC bought 225 metric tonnes of the yellow metal—the most among global central banks, according to the World Gold Council.

China’s purchases last year were about a quarter of the 1,037 tonnes bought by all the world’s central banks. In January and February this year alone, the PBC increased its gold reserves by 22 tonnes. It has been adding to its gold reserves for the past 17 months. The Chinese central bank’s total gold holdings stand at about 2,257 tonnes.

What explains Beijing’s love for bullion?

Experts put this down to its battle of supremacy with the US and the broad trend of de-dollarization.

Beijing, which has over the decades built huge forex reserves in dollars, is now seeking to diversify its holdings and insulate its financial sector.

China, like most countries, is heavily dependent on the US dollar for global trade. The greenback is the world’s reserve currency and holds a virtual monopoly in the global financial architecture. However, as the covid-19 crisis and Russia-Ukraine war showed, Washington does not shy away from weaponizing the dollar to sanction countries and maintain its hegemony.

Beijing, which has over the decades built huge forex reserves in dollars, is now seeking to diversify its holdings and insulate its financial sector.

“China is the largest producer of gold in the world, but its central bank has still been at the forefront of a surge in purchases of the precious metal on the international market since past 17 consecutive months as it seeks to reduce its reliance on the dollar and diversify its holdings in reserves,” AnandRathi’s Mathur said.

“Its gold rush could also be an attempt to shore up its fiscal position with a stable and highly saleable asset as bond markets have suffered since 2022,” he added.

Flashing red?

The current trend of gold buying is not limited to China. All central banks are stocking up on this asset.

Prior to 2022, there wasn’t a single year when global central banks cumulatively bought 1,000 tonnes of gold. But in 2022 and 2023, central bank purchases stood at 1,081 tonnes and 1,037 tonnes, respectively.

When central banks buy gold, it is usually a carefully considered strategic move. They don’t buy gold for short-term trading or profit-booking. It is either to safeguard their currencies, diversify their reserves or hedge geopolitical risks. Sometimes all of the above.

This is what is making many market watchers nervous.

Does the scale of gold buying indicate central banks are not quite gung-ho about the future? Do they know something the rest of the market does not? Remember, central banks are the most sophisticated institutions in the global financial landscape.

“There is a rising risk regarding war. New ‘Iron Curtains’ are being built unfortunately. The gold price is perhaps also signalling that the next wave of inflation is starting,” Incrementum AG’s Stöferle said.

View Full Image

Gold is possibly a more accurate ‘fear gauge’ than VIX—the Chicago Board Options Exchange’s CBOE Volatility Index, which is the most popular measure of the stock market’s expectation of volatility.

Here’s a snapshot of the previous times when the yellow metal hit lifetime highs—1970s (after the ‘Nixon shock’ ended the convertibility of the US dollar to gold); 2008 (global financial crisis); 2011 (European debt crisis) and 2020 (covid-19 outbreak).

Correlation does not mean causation, of course, but it is safe to say shining gold prices have almost always been accompanied by some very grim news.

What is the bullion market nervous about currently? The risk of a wider conflagration in the Middle East? Sabre rattling by Vladimir Putin and Xi Jinping? The US-China rivalry spiralling into a major showdown? Or is it betting that the US economy will not achieve a ‘soft landing’, no matter how buoyant Fed chair Jerome Powell sounds?

The correct answer(s) will be known only in hindsight, but experts are voicing some concern about the medium-term outlook.

Correlation does not mean causation, of course, but it is safe to say shining gold prices have almost always been accompanied by some very grim news.

“The probability of a hard landing in the US economy this year still persists given the fact that historically, the Fed has managed a soft landing only twice following nine previous tightening cycles over the past five decades. The other seven had ended in a recession making a hard landing scenario still feasible this year,” Mathur added.

Domestic doubts

View Full Image

Gold buyers in emerging markets like India have to contend with an additional factor which exerts upward pressure on prices—currency depreciation.

The rupee has been weakening against the US dollar, in line with most emerging market currencies, which makes purchases of dollar-priced commodities like crude oil and gold more expensive.

Gold prices breached the ₹72,000 per 10gm mark, while silver topped ₹84,000 per kg on 12 April—both record highs. The yellow metal is up around 15% year-to-date.

That said, India’s age-old cultural affinity with gold makes demand pretty inelastic.

Indian gold demand, which has been in the range of 700-800 tonnes annually since 2019, is expected to increase to 800-900 tonnes in 2024 on the back of robust economic growth and higher income, as per the World Gold Council.

However, for investors itching to participate in the red-hot rally, caution is the keyword.

“While transition to lower interest rates bodes well for gold, much of it seems to have already been priced in. This could limit the upside for the precious metal going forward,” said Chirag Mehta, chief investment officer, and Ghazal Jain, fund manager, Quantum AMC.

Further, meaningful upside from these levels can come on the back of a more dovish stance by the US central bank in response to a sharp deceleration in growth or a financial accident.

“On the other hand, if the Fed doesn’t meet the market’s expectations with regards to quantum and timing of rate cuts, given that inflation continues to be sticky above its target, gold could see some consolidation,” they added.